The book that played a pivotal role in shaping my understanding of monetary economics is now available online at no cost: Less Than Zero by George Selgin. Among other things, this book will help one (1) appreciate why stabilizing nominal spending should be the ultimate objective of monetary policy and (2) why the deflationary pressures of 2009 were very different than those of 2003.

Macro Musings Blog

Thursday, November 26, 2009

A Good Time at the SEA Annual Meetings

Earlier this week I attended the Southern Economic Association annual meetings in San Antonio, Texas. Among other things, I was part of a session at the meetings whose participants all happen to agree the Fed let the ball drop in late 2008, early 2009 by effectively--though not intentionally--letting monetary policy tighten: George Selgin, Scott Sumner, Josh Hendrickson, and of course myself. (See here and here for evidence of this tightening.) Our session went well (Larry H. White agrees) and we were able to chat some more over meals along the riverwalk. The conversations were great and covered everything from blogging to nominal income targeting to fiscal policy. I left the meetings more convinced than ever that a nominal income target would have done a lot to prevent the crisis--in terms of minimizing the buildup of economic imbalances during the 2003-2005 nominal spending boom as well as the late 2008, early 2009 nominal spending collapse--and is the best way forward for U.S. monetary policy given the current institutional arrangements in the United States. I want to thank Josh Hendrickson for organizing the session.

Monday, November 16, 2009

Assorted Monetary Musings

Here are some assorted monetary musings:

(1) Paul Krugman comes clean and acknowledges unconventional monetary policy can still pack a punch. In fact, he says the "first-best answer" to our current economic crisis is not expansionary fiscal policy, but a credible commitment by the Federal Reserve to higher inflation. An exasperated Scott Sumner who has been making this case for some time wonders why Krugman has taken so long to acknowledge this point. Krugman replies that he has not pushed this idea because he believes it will not get any traction. As a result he turned to expansionary fiscal policy as a second-best solution. In other words, Krugman believes he faces the following tradeoff regarding aggregate demand-stabilizing policies:

Krugman may be right on this policy tradeoff. But given Krugman's immense political influence, he could have made this issue front and central for policymakers. And with enough exposure unconventional moneary policy could have become a first-best political solution too. In short, had Krugman been pushing this idea some time ago it may have gone a long way in preventing the collapse in nominal spending over the past year. Moving forward, it is good to remember that it was unconventional monetary policy (and not fiscal policy) that ended the Great Contraction of 1929-1933. So too can it now keep the U.S. economy from entering a prolonged slump.

Krugman may be right on this policy tradeoff. But given Krugman's immense political influence, he could have made this issue front and central for policymakers. And with enough exposure unconventional moneary policy could have become a first-best political solution too. In short, had Krugman been pushing this idea some time ago it may have gone a long way in preventing the collapse in nominal spending over the past year. Moving forward, it is good to remember that it was unconventional monetary policy (and not fiscal policy) that ended the Great Contraction of 1929-1933. So too can it now keep the U.S. economy from entering a prolonged slump.

2. Speaking of Scott Sumner, I did a long run yesterday and listened to his podcast with Russ Roberts to pass the time. It was good interview and covered many of the same issues Scott has made on his blog. One of the points he made is that monetary policy could improve its ability to stabilize the macroeconomy by targeting some measure of nominal spending. I too am an advocate of the Federal Reserve stabilizing nominal spending for the same reasons. However, I am a little less confident that it is always a sufficient policy response in terms of stabilizing the macroeconomy. For example, if we look at the period called the "Great Moderation" that occurred during the 25+ years prior to the current crisis, we see the Federal Reserve did a fairly good job on average of stabilizing nominal spending around 5% growth (See this figure). However, this time was also a period of the Fed asymmetrically responding to swings in asset prices. Asset prices were allowed to soar to dizzying heights and always cushioned on the way down with an easing of monetary policy. This behavior by the Fed appears in retrospect to have caused observers to underestimate aggregate risk and become complacent. It also probably contributed to the increased appetite for the debt during this time. These developments all contributed to current crisis. To the extent, then, that stabilizing nominal spending requires the Fed to respond as it did to swings in asset prices during this time, then it becomes less clear to me that targeting nominal spending is always a sufficient condition for macroeconomic stability. Don't get me wrong, I still believe a nominal spending target would have done much to prevent the collapse in nominal spending over the past year and ultimately it would be an improvement over current Fed policy. The gradual buildup of excesses during the "Great Moderation", though, suggest to me that something more is needed. That is why I see a two part approach to macroeconomic stability: (1) target nominal spending and (2) implement macroprudential regulations.

2. It was a really long run so I also listened to a podcast where Bloomberg's Tom Keene interviewed Bruce Bartlett about his new book The New American Economy. It was an interesting interview, but at one point Bartlett claimed there was nothing more monetary policy could for the economy at this point. Apparently, Bartlett has not been reading Scott Sumner's blog. Bartlett also said of all economists he finds Krugman to make the most sense on the current crisis. If so, then there is hope for Bartlett given Krugman's admission that unconventional monetary policy can still work as noted above.

3. Bill Woolsely has had some great recent posts on monetary economics. First, he reminds us that we should not confuse money with credit. Second, he responds to Bryan Caplan's post on velocity by, among other things, coming to defense of the equation of exchange as being more than a trivial tautology. I agree with him that the equation of exchange is useful in thinking about monetary economics and have used it here before on this blog.

4. Francois R. Velde has a new paper on the recession of 1937. It is probably the best paper I have seen on the on this recession and makes a great policy implication for today: beware of tightening policy too soon in the recovery. Below is a figure from the paper that shows a historical decomposition of the recession. It comes from a vector autoregression that decomposes or attributes the forecast error for industrial production into non-forecasted movements in other series. Here, the other series are monetary policy as measured by M1, fiscal policy as measured by fiscal balance, and labor costs as measured by wages. In this figure, these series contribution to the forecast error--the difference between actual and forecasted (i.e. baseline) values-- of industrial production is shown by their own colored lines. For example, the closer the baseline + M1 line is to the solid black line (i.e. actual industrial production) the more of the forecast error is explained by monetary policy: (Click on figure to enlarge)

This figure makes clear that tight monetary and fiscal policy explain most of the 1937 recession. Read the paper here.

(1) Paul Krugman comes clean and acknowledges unconventional monetary policy can still pack a punch. In fact, he says the "first-best answer" to our current economic crisis is not expansionary fiscal policy, but a credible commitment by the Federal Reserve to higher inflation. An exasperated Scott Sumner who has been making this case for some time wonders why Krugman has taken so long to acknowledge this point. Krugman replies that he has not pushed this idea because he believes it will not get any traction. As a result he turned to expansionary fiscal policy as a second-best solution. In other words, Krugman believes he faces the following tradeoff regarding aggregate demand-stabilizing policies:

Krugman may be right on this policy tradeoff. But given Krugman's immense political influence, he could have made this issue front and central for policymakers. And with enough exposure unconventional moneary policy could have become a first-best political solution too. In short, had Krugman been pushing this idea some time ago it may have gone a long way in preventing the collapse in nominal spending over the past year. Moving forward, it is good to remember that it was unconventional monetary policy (and not fiscal policy) that ended the Great Contraction of 1929-1933. So too can it now keep the U.S. economy from entering a prolonged slump.

Krugman may be right on this policy tradeoff. But given Krugman's immense political influence, he could have made this issue front and central for policymakers. And with enough exposure unconventional moneary policy could have become a first-best political solution too. In short, had Krugman been pushing this idea some time ago it may have gone a long way in preventing the collapse in nominal spending over the past year. Moving forward, it is good to remember that it was unconventional monetary policy (and not fiscal policy) that ended the Great Contraction of 1929-1933. So too can it now keep the U.S. economy from entering a prolonged slump.2. Speaking of Scott Sumner, I did a long run yesterday and listened to his podcast with Russ Roberts to pass the time. It was good interview and covered many of the same issues Scott has made on his blog. One of the points he made is that monetary policy could improve its ability to stabilize the macroeconomy by targeting some measure of nominal spending. I too am an advocate of the Federal Reserve stabilizing nominal spending for the same reasons. However, I am a little less confident that it is always a sufficient policy response in terms of stabilizing the macroeconomy. For example, if we look at the period called the "Great Moderation" that occurred during the 25+ years prior to the current crisis, we see the Federal Reserve did a fairly good job on average of stabilizing nominal spending around 5% growth (See this figure). However, this time was also a period of the Fed asymmetrically responding to swings in asset prices. Asset prices were allowed to soar to dizzying heights and always cushioned on the way down with an easing of monetary policy. This behavior by the Fed appears in retrospect to have caused observers to underestimate aggregate risk and become complacent. It also probably contributed to the increased appetite for the debt during this time. These developments all contributed to current crisis. To the extent, then, that stabilizing nominal spending requires the Fed to respond as it did to swings in asset prices during this time, then it becomes less clear to me that targeting nominal spending is always a sufficient condition for macroeconomic stability. Don't get me wrong, I still believe a nominal spending target would have done much to prevent the collapse in nominal spending over the past year and ultimately it would be an improvement over current Fed policy. The gradual buildup of excesses during the "Great Moderation", though, suggest to me that something more is needed. That is why I see a two part approach to macroeconomic stability: (1) target nominal spending and (2) implement macroprudential regulations.

2. It was a really long run so I also listened to a podcast where Bloomberg's Tom Keene interviewed Bruce Bartlett about his new book The New American Economy. It was an interesting interview, but at one point Bartlett claimed there was nothing more monetary policy could for the economy at this point. Apparently, Bartlett has not been reading Scott Sumner's blog. Bartlett also said of all economists he finds Krugman to make the most sense on the current crisis. If so, then there is hope for Bartlett given Krugman's admission that unconventional monetary policy can still work as noted above.

3. Bill Woolsely has had some great recent posts on monetary economics. First, he reminds us that we should not confuse money with credit. Second, he responds to Bryan Caplan's post on velocity by, among other things, coming to defense of the equation of exchange as being more than a trivial tautology. I agree with him that the equation of exchange is useful in thinking about monetary economics and have used it here before on this blog.

4. Francois R. Velde has a new paper on the recession of 1937. It is probably the best paper I have seen on the on this recession and makes a great policy implication for today: beware of tightening policy too soon in the recovery. Below is a figure from the paper that shows a historical decomposition of the recession. It comes from a vector autoregression that decomposes or attributes the forecast error for industrial production into non-forecasted movements in other series. Here, the other series are monetary policy as measured by M1, fiscal policy as measured by fiscal balance, and labor costs as measured by wages. In this figure, these series contribution to the forecast error--the difference between actual and forecasted (i.e. baseline) values-- of industrial production is shown by their own colored lines. For example, the closer the baseline + M1 line is to the solid black line (i.e. actual industrial production) the more of the forecast error is explained by monetary policy: (Click on figure to enlarge)

This figure makes clear that tight monetary and fiscal policy explain most of the 1937 recession. Read the paper here.

Monday, November 9, 2009

Further Readings on Nominal Spending

Given all the interest my figures generated on stabilizing nominal spending as a policy goal, I thought I would follow up with a collection of links to my posts and others on this topic. Let me note up front that stabilizing nominal spending as goal is nothing new and has been promoted in the past by many prominent economists such as Greg Mankiw, Robert Hall, Bennett McCallum, and others in the form of a nominal income targeting rule. It is just that this current crisis has sparked a renewed interest in the idea, at least among some observers.

Here are some blog posts:

(1) Why Care About Nominal Spending?--David Beckworth

(2) More on the Importance of Nominal Spending Shocks--David Beckworth

(3) Why Nominal GDP Matters--Scott Sumner

(4) Recognizing the Nature of the Macro Problem in My Views on Money/Macro--Scott Sumner

(5) Why Current AD Depends on Expected Future AD--Nick Rowe

And here are some accessible academic articles:

(1) Understanding Nominal GDP Targeting--Michael Bradley and Dennis Jansen

(2) Nominal Income Targeting--Greg Mankiw and Robert Hall

There are many other academic articles on nominal income targeting but most are highly technical. If you know of any more introductory or survey-type articles on this topic please let me know.

Here are some blog posts:

(1) Why Care About Nominal Spending?--David Beckworth

(2) More on the Importance of Nominal Spending Shocks--David Beckworth

(3) Why Nominal GDP Matters--Scott Sumner

(4) Recognizing the Nature of the Macro Problem in My Views on Money/Macro--Scott Sumner

(5) Why Current AD Depends on Expected Future AD--Nick Rowe

And here are some accessible academic articles:

(1) Understanding Nominal GDP Targeting--Michael Bradley and Dennis Jansen

(2) Nominal Income Targeting--Greg Mankiw and Robert Hall

There are many other academic articles on nominal income targeting but most are highly technical. If you know of any more introductory or survey-type articles on this topic please let me know.

Friday, November 6, 2009

My Reply to Krugman

Paul Krugman has chimed in on my figure showing the collapse in nominal spending. He, however, is less enthusiastic about its implications:

And if inflationary expectations had not collapse then current nominal spending would have been far more stable. This is because if folks think that inflation will be permanently higher going forward they are more likely to spend their money today. That is, money demand will fall and velocity will pick up.

This is a point I empirically tested in a recent post. There I took the monthly expected inflation series implied by the difference between the nominal 10-year Treasury yield and the 10-year TIPs yield and put it in a vector autoregression (VAR) along with the monthly GDP series from macroeconomic advisers. Nominal GDP was turned into an annualized monthly growth rate and the data used runs from 1999:1 through 2007:9. More data would have been helpful, but TIPs only start in the late 1990s.* The two figures below show what the typical responses of expected inflation and nominal GDP to the typical sudden change or shock to expected inflation over the sample. The solid line shows the point estimate while the dashed lines show two standard deviations around the point estimate. Upon impact, the shock causes expected inflation to jump 16 basis points and occurs as the level of nominal GDP increases by 1.16 percent. In other words, a sudden positive change in expected inflation is associated with an increase in current nominal spending. Both effects persist but eventually become insignificant about 14-15 months later. (Click on figures to enlarge.)

So contrary to Krugman's claim, there is reason to believe the Fed could have prevented the great nominal spending crash of 2008-2009. The real question for me is why did the Fed allow inflationary expectations to fall so dramatically in late 2008, early 2009. My guess is they simply dropped the ball or there was too much pressure from inflationary hawks.

So contrary to Krugman's claim, there is reason to believe the Fed could have prevented the great nominal spending crash of 2008-2009. The real question for me is why did the Fed allow inflationary expectations to fall so dramatically in late 2008, early 2009. My guess is they simply dropped the ball or there was too much pressure from inflationary hawks.

Update I: The Economist blog Free Exchange responds to Krugman's post by arguing that monetary policy is not out of gas.

Update II: Scott Sumner also shoots down Krugman's nominal nonsense.

[The figure is] certainly suggestive. But I disagree with the interpretation that this shows that the current slump is mainly about insufficiently expansionary monetary policy...Note that the part about changing expectations of future inflation in parentheses is actually an admission that monetary policy can do something about the current slump. Krugman, however, does not explore this point anywhere else in his post. That is unfortunate because it is the very argument advocates like Scott Sumner have been making in their case that monetary policy could have done more to prevent the nominal spending crash of 2008-2009. One way to think about this is to imagine what would have happened had the Fed set an explicit inflation target of say 3% in mid-2008 and promised it would do whatever was needed to keep actual inflation there. If such a policy had been adopted it is unlikely inflation expectations would have collapsed liked they did in late 2008, early 2009 as seen in the figure below (click on figure to enlarge):

[...]

Focusing on nominal spending makes you think that low nominal spending is the problem, a problem with a monetary solution; but actually it’s the symptom, and monetary policy doesn’t matter (unless it can affect expected future inflation, but that’s another story).

And if inflationary expectations had not collapse then current nominal spending would have been far more stable. This is because if folks think that inflation will be permanently higher going forward they are more likely to spend their money today. That is, money demand will fall and velocity will pick up.

This is a point I empirically tested in a recent post. There I took the monthly expected inflation series implied by the difference between the nominal 10-year Treasury yield and the 10-year TIPs yield and put it in a vector autoregression (VAR) along with the monthly GDP series from macroeconomic advisers. Nominal GDP was turned into an annualized monthly growth rate and the data used runs from 1999:1 through 2007:9. More data would have been helpful, but TIPs only start in the late 1990s.* The two figures below show what the typical responses of expected inflation and nominal GDP to the typical sudden change or shock to expected inflation over the sample. The solid line shows the point estimate while the dashed lines show two standard deviations around the point estimate. Upon impact, the shock causes expected inflation to jump 16 basis points and occurs as the level of nominal GDP increases by 1.16 percent. In other words, a sudden positive change in expected inflation is associated with an increase in current nominal spending. Both effects persist but eventually become insignificant about 14-15 months later. (Click on figures to enlarge.)

So contrary to Krugman's claim, there is reason to believe the Fed could have prevented the great nominal spending crash of 2008-2009. The real question for me is why did the Fed allow inflationary expectations to fall so dramatically in late 2008, early 2009. My guess is they simply dropped the ball or there was too much pressure from inflationary hawks.

So contrary to Krugman's claim, there is reason to believe the Fed could have prevented the great nominal spending crash of 2008-2009. The real question for me is why did the Fed allow inflationary expectations to fall so dramatically in late 2008, early 2009. My guess is they simply dropped the ball or there was too much pressure from inflationary hawks.Update I: The Economist blog Free Exchange responds to Krugman's post by arguing that monetary policy is not out of gas.

Update II: Scott Sumner also shoots down Krugman's nominal nonsense.

*(Technical note: both series were in rates so no unit root problems, 13 lags were used to eliminate serial correlation, and corporate bond spreads were included as a control variable for the financial crisis).

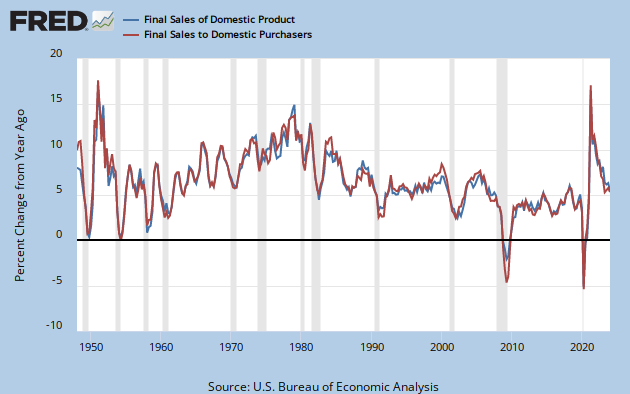

Why Care About Nominal Spending?

Thanks to Alex Tabarrok, The Economist's Free Exchange blog, Ezra Klein, and Bruce Bartlett my last post on the history of U.S. nominal spending received a lot of attention. It also raised the important question of why we should care about nominal spending. Before I answer this question let me first define nominal spending: it is the current dollar value of total spending in an economy. More simply, it is total demand in an economy. Technically, what I showed in the last post was the growth rate of final sales to domestic purchasers or U.S. domestic demand. One could also look at final sales of domestic product--which includes foreign purchases of U.S. made goods and services--which is aggregate demand for the U.S. economy. Either way, both series show a large collapse in nominal spending late 2008, early 2009 as seen in this figure.

Now on to the importance of nominal spending. I have asserted that the best way for the Fed to reduce macroeconomic volatility is to stabilize nominal spending rather than inflation. Here is why. If an economy is running at full employment, then any sudden increase or decrease in nominal spending will give rise to changes in real economic activity that are not sustainable. This is because there are numerous rigidities that prevent prices from adjusting instantly. There is simply no way to suddenly jar nominal spending (i.e. create a nominal spending shock) and not have real economic activity move as well.

{kind=link}

Now on to the importance of nominal spending. I have asserted that the best way for the Fed to reduce macroeconomic volatility is to stabilize nominal spending rather than inflation. Here is why. If an economy is running at full employment, then any sudden increase or decrease in nominal spending will give rise to changes in real economic activity that are not sustainable. This is because there are numerous rigidities that prevent prices from adjusting instantly. There is simply no way to suddenly jar nominal spending (i.e. create a nominal spending shock) and not have real economic activity move as well.

Note that the key here is not to aim for inflation stability, but to aim for nominal spending stability. This is because inflation is merely a symptom of nominal spending shocks. Moreover, inflation can sometimes can be hard to interpret--Is the high (low) inflation due to positive (negative) aggregate demand (AD) shocks or negative (positive) aggregate supply shocks (AS)?--and as a result monetary policy that targets inflation rather than nominal spending may make the wrong call. To illustrate this point, consider the following two cases*:

(1) A central bank has a 2% inflation target and the economy's sustainable (i.e. natural) rate of growth is 3%. Here we have nominal spending growing at 5%. Now imagine that fiscal policy generates a positive AD shock that increases nominal spending and pushes inflation temporarily to 4%. Now nominal spending is growing at 7% and if there are any nominal rigidities (i.e. upward slopping SRAS curve) this increase in nominal spending (or AD) should also push real economic activity beyond its natural rate. Hence, a positive output gap is created and there is an uptick in inflation. In this scenario--where a positive AD shock is the issue--a policy aiming to stabilize nominal spending would have prevented the output gap from emerging. An inflation target regime would have also addressed the output gap, but since inflation is a symptom of the nominal spending shock it only would have done so after the horse was out of the barn, so to speak. Still, in this case inflation targeting would have made the right call.There are other scenarios one could consider, but any way you slice it what becomes apparent is that monetary policy that targets nominal spending can handle both AD and AS supply shocks, while monetary policy that targets inflation can only handle AD shocks. I believe one example of this was the 2003-2004 period when the U.S. economy was buffeted with rapid productivity gains (i.e. positive AS shocks) that led to low inflation. The Fed interpreted this low inflation as indicating weak AD and kept monetary policy extremely loose. They were wrong, nominal spending was soaring by 2003 and thus, monetary policy was too accommodative. I also believe that had the Fed been targeting nominal spending it would been easier for them to avoid the collapse in nominal spending that occurred in late 2008, early 2009. Of course, an explicit inflation target would have helped too but why not go for root of the problem rather than its symptom?

(2) A central bank has a 2% inflation target and the economy's natural rate of growth is 3%. Once again, nominal spending is growing at 5%. Now assume a permanent productivity innovation pushes the natural rate of real economic growth to 5%. Assume also that the surge in productivity in the absence of any new accommodation or changes in monetary policy--that is, the central bank is still increasing money supply at rate that would have created a 2% inflation target under the old steady state of 3% real growth--would have pushed inflation down to 0%. If the central bank adopts this approach and does not accommodate the increase in productivity, nominal spending will still be at 5% (0% inflation + 5% real growth). Note, there has been no change in AD (still growing at 5%) and thus no movements against the SRAS by which to create an output gap.

Now assume the central doesn't sit idly by but accommodates the productivity shock so that its inflation target is maintained. It will have to stimulate nominal spending such that the potential 2% drop in inflation is avoided. Now nominal spending jumps to 7% from its previous value of 5%. Here, we have a sudden increase in nominal spending (or AD) that in the face of an upward-slopping SRAS will temporarily push output beyond its natural rate. In other words, an positive output gap will emerge. But here there is no observed change in inflation or the inflation target! Had the central bank targeted a 5% nominal spending growth rate this output gap would not have emerged. Instead, its rigid focus on inflation caused it to be too accommodative.

For more on the importance of stabilizing nominal spending I would recommend you take a look at Scott Sumner's blog. Also, here is an article from the St. Louis Fed that provides a more thorough but gentle introduction to the importance of nominal spending and how monetary policy might target it.

* These are variations of scenarios I first posted over at Worthwhile Canadian Initiative.

Tuesday, November 3, 2009

Global Nominal Spending History

As someone who believes that stabilizing nominal spending rather than inflation is key to macroeconomic stability, I have taken the liberty in the past to reframe U.S. macroeconomic history according to this perspective. Thus, I renamed (1) the "Great Inflation" that started in the mid-1960s and ended in the early-1980s as the "Great Nominal Spending Spree" and (2) the "Great Moderation" of 25 years or so preceding the current crisis the "Great Moderation in Nominal Spending." I also labeled the late-2008, early 2009 period as the "Great Nominal Spending Crash". Below was the figure I used to summarize this reframing of U.S. macroeconomic history (Click on figure to enlarge):

Recently, I learned the OECD has a quarterly nominal GDP measure (PPP-adjusted basis) aggregated across 25 of its member countries going back to 1960:Q1. The countries are as follows: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Greece, Iceland, Ireland, Italy, Japan, Luxembourg, Mexico, Netherlands, New Zealand, Norway, Portugal, Spain, Sweden, Switzerland, Turkey, United Kingdom and United States. The combined economies of these counties make up over half the world economy and thus, provide some sense of global nominal spending. So in the spirit of reframing global macroeconomic history according to a nominal spending perspective I created the following figure (click on figure to enlarge):

I suspect the similarities between these two figures speak to the size and influence of the U.S. economy. I think it also speaks to the influence of U.S. monetary policy on global liquidity conditions and, thus, it influence on global nominal spending.

Recently, I learned the OECD has a quarterly nominal GDP measure (PPP-adjusted basis) aggregated across 25 of its member countries going back to 1960:Q1. The countries are as follows: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Greece, Iceland, Ireland, Italy, Japan, Luxembourg, Mexico, Netherlands, New Zealand, Norway, Portugal, Spain, Sweden, Switzerland, Turkey, United Kingdom and United States. The combined economies of these counties make up over half the world economy and thus, provide some sense of global nominal spending. So in the spirit of reframing global macroeconomic history according to a nominal spending perspective I created the following figure (click on figure to enlarge):

I suspect the similarities between these two figures speak to the size and influence of the U.S. economy. I think it also speaks to the influence of U.S. monetary policy on global liquidity conditions and, thus, it influence on global nominal spending.

Monday, November 2, 2009

Pick Your Poison

After reading Nouriel Roubini's latest article in the FT I feel less certain about what the Fed should be doing going forward. On one hand I see figures like the one below from the IMF's World Economic Outlook (p. 32) that point to excess global capacity and the ongoing threat of global deflation (the bad kind) and come to same conclusion as Scott Sumner:

On the other hand, Nouriel Roubini claims the current Fed policies in conjunction with a large dollar carry trade is creating a new set of asset bubbles:

If the Fed adopted a much more expansionary monetary policy, and if the PBOC kept its policy stance the same, then world monetary policy would become more expansionary, and world aggregate demand would increase. That would help everyone.In short, the Fed should use its monetary superpower status to ensure there is ample global liquidity and in so doing stabilize global nominal spending.

On the other hand, Nouriel Roubini claims the current Fed policies in conjunction with a large dollar carry trade is creating a new set of asset bubbles:

Risky asset prices have risen too much, too soon and too fast compared with macroeconomic fundamentals... So what is behind this massive rally? Certainly it has been helped by a wave of liquidity from near-zero interest rates and quantitative easing. But a more important factor fueling this asset bubble is the weakness of the US dollar, driven by the mother of all carry trades. The US dollar has become the major funding currency of carry trades as the Fed has kept interest rates on hold and is expected to do so for a long time.Investors who are shorting the US dollar to buy on a highly leveraged basis higher-yielding assets and other global assets are not just borrowing at zero interest rates in dollar terms; they are borrowing at very negative interest rates – as low as negative 10 or 20 per cent annualised – as the fall in the US dollar leads to massive capital gains on short dollar positions.Roubini is not optimistic about what this means for the future:Let us sum up: traders are borrowing at negative 20 per cent rates to invest on a highly leveraged basis on a mass of risky global assets that are rising in price due to excess liquidity and a massive carry trade. Every investor who plays this risky game looks like a genius – even if they are just riding a huge bubble financed by a large negative cost of borrowing – as the total returns have been in the 50-70 per cent range since March.

People’s sense of the value at risk (VAR) of their aggregate portfolios ought, instead, to have been increasing due to a rising correlation of the risks between different asset classes, all of which are driven by this common monetary policy and the carry trade. In effect, it has become one big common trade – you short the dollar to buy any global risky assets.

Yet, at the same time, the perceived riskiness of individual asset classes is declining as volatility is diminished due to the Fed’s policy of buying everything in sight – witness its proposed $1,800bn (£1,000bn, €1,200bn) purchase of Treasuries, mortgage- backed securities (bonds guaranteed by a government-sponsored enterprise such as Fannie Mae) and agency debt. By effectively reducing the volatility of individual asset classes, making them behave the same way, there is now little diversification across markets – the VAR again looks low.

So the combined effect of the Fed policy of a zero Fed funds rate, quantitative easing and massive purchase of long-term debt instruments is seemingly making the world safe – for now – for the mother of all carry trades and mother of all highly leveraged global asset bubbles.

[O]ne day this bubble will burst, leading to the biggest co-ordinated asset bust ever: if factors lead the dollar to reverse and suddenly appreciate – as was seen in previous reversals, such as the yen-funded carry trade – the leveraged carry trade will have to be suddenly closed as investors cover their dollar shorts. A stampede will occur as closing long leveraged risky asset positions across all asset classes funded by dollar shorts triggers a co-ordinated collapse of all those risky assets – equities, commodities, emerging market asset classes and credit instruments.So what is the bigger threat: global deflation or asset bubbles driven by Fed policy and "the mother of all carry trades"? Tim Lee via Buttonwood also sees potential problems to the unwinding of this dollar carry trade. I hope there is another way out for the Fed.

Subscribe to:

Posts (Atom)